The Profit Margin: November 10, 2025

Statistic of the Week

The age of first-time homebuyers in the U.S. continues to rise. In 1991, the median age was 28, it was 30 in 2010, and increased to 33 by 2019. This year, it climbed to 40 for the first time on record. Repeat buyers have also aged, with the median age rising from 42 in 1991 to 62 this year.

Global Perspective

The Bank of England kept its benchmark interest rate at 4.00% in a close 5–4 vote, with dissenting members favoring a 0.25% cut. Markets anticipate a rate reduction at the Bank’s December meeting. The BOE noted that consumer inflation is “judged to have peaked” at 3.8% in September.

Market Moving Events

Tuesday: Veteran’s Day – Bond Market Closed

Thursday: Jobless Claims*, CPI*, Federal Budget

Friday: Retail Sales*, PPI*, Business Inventories*

*Denotes data unlikely to be released if federal government remains closed.

Commentary

November has historically been the best month for equities. This November, volatility seems to be the theme. Market sentiment cooled last week as investors weighed corporate earnings and a range of alternative labor market data. The Nasdaq led declines, falling 3.04%, its worst week since April.1 Meanwhile, the S&P 500 slipped 1.63% and the DJIA dipped 1.21%.2 Notably, both the Nasdaq and S&P rebounded on Friday to close above their critical 50-day moving averages.3 Bond yields edged higher to the chagrin of fixed income investors, with the 10-year Treasury finishing the week at 4.10%, up 0.03% from the week prior.4

With the federal government shut down, key labor and inflation data, widely considered the “gold standard,” remain unavailable. As a result, investors have been piecing together insights from alternative sources. The ADP report exceeded expectations, showing 42,000 new jobs in October.5 Citi and Goldman Sachs estimate weekly jobless claims are holding just below 230,000,6 while the Chicago Fed projects the October unemployment rate rose to 4.36%.7 The frequently overlooked Challenger, Gray & Christmas report garnered headlines when it showed roughly 1.1 million layoffs year-to-date – a 175% increase from last year.8 Overall, the data present a mixed picture toward signs of a weakening labor market.

Several Federal Reserve officials are scheduled to speak this week. Their remarks on the labor market and inflation will be closely monitored. The earnings season continues. Importantly, even if the government reopens, the CPI and PPI releases are unlikely to occur as scheduled.

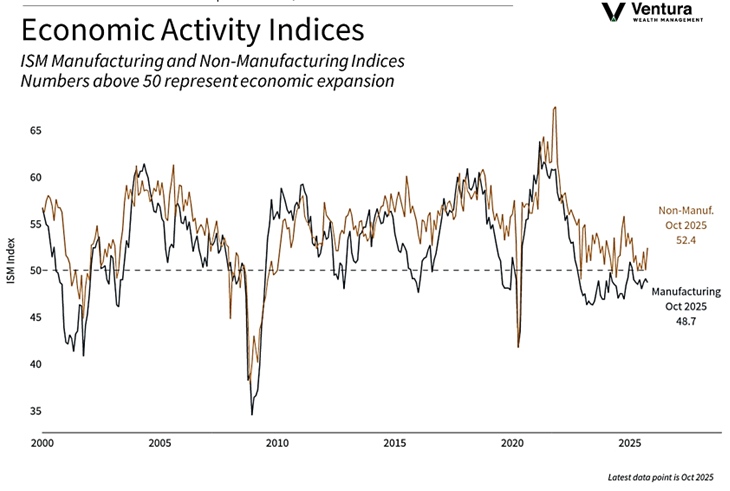

Chart of the Week

The ISM Manufacturing and Non-Manufacturing (Services) Activity Indices beat analyst expectations last week. The Services Index remains firmly in expansion territory above 50, while the Manufacturing Index reflects continued weakness

Source Materials

Market Moving Events:

MarketWatch.com

Chart of the Week:

Clearnomics,

Institute for Supply Management

Statistic of the Week:

The New York Times, Barron’s

Global Perspective:

The Economist

Commentary:

1. Bloomberg

2. Bloomberg

3. Bloomberg

4. MarketWatch.com

5. Barron’s

6. Morningstar, MarketWatch.com

7. Barron’s

8. MarketWatch.com