The Profit Margin: June 16, 2025

Statistic of the Week

In May, exports from China to the U.S. experienced a sharp decline. Year-over-year, Chinese exports dropped by 34.5%, marking the largest decrease since February 2020, when the pandemic severely disrupted global trade. However, overall Chinese exports rose by 5% in May, with a notable 12% increase in exports to the European Union compared to the previous year.

Global Perspective

Last week in London, the United States and China reached a preliminary agreement regarding trade discussions. Although the most crucial negotiations are yet to come, the U.S. will continue to impose a 55% tariff on imports from China. This total includes the existing 25% tariffs, an additional 10% in reciprocal tariffs, and a 20% tariff related to fentanyl smuggling. Meanwhile, China has committed to enhancing U.S. access to rare earth minerals.

Market Moving Events

Tuesday: Retail Sales, Import Prices, Home Builder Confidence

Wednesday: Housing Starts, Jobless Claims, FOMC Meeting Announcement

Thursday: U.S. Markets and VWM Closed

Friday: Leading Economic Indicators

Commentary

Domestic equity markets were performing well last week until Israel’s attack on Iran in “Operation Rising Lion.” All three major averages flipped from positive to negative weekly performance on the news. Of the major averages, the S&P 500 held up the best on the week. It retreated below 6,000 yet only logged a weekly decline of 0.39%.1 The Nasdaq fell 0.63%.2 And the DJIA faired the worst. It dipped 1.32%.3 Investors sought out safety in U.S. Treasuries. The yield on the 10-year Treasury fell 0.11% to finish the week with a yield of 4.41%.4 While bonds and gold rallied as they were perceived as “safe haven” assets, it is interesting to note that the dollar remains under significant pressure.5 Typically the dollar would rise in a time of uncertainty / global conflict.

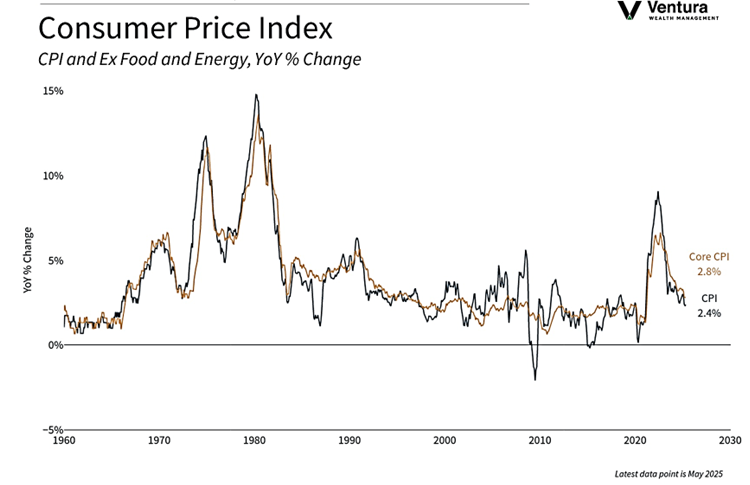

Trading action is likely to be choppy this week, with the ongoing conflict and markets closed Thursday for Juneteenth. The FOMC will have a meeting announcement on Wednesday. Markets are not expecting a rate cut.6 While inflation data has been improving (chart right), the Fed is likely to cite the administration’s tariff policy as a reason to leave rates unchanged. Add to the tariffs a spike in oil prices (West Texas was up 8.3% on Friday),7 and it is likely that more dovish members of the FOMC will sit on the sidelines.

We will also receive the Retail Sales and Initial Jobless Claims reports. Retail sales are forecasted to have contracted slightly in May, led lower by weak auto sales.8 Jobless Claims have been trending higher. This is a trend that will need to be closely monitored.

Chart of the Week

In May, the Consumer Price Index increased by 0.1%, coming in below expectations. The annual inflation rate currently stands at 2.4%. Additionally, the core readings were lower than predicted.

Source Materials

Market Moving Events:

MarketWatch.com

Chart of the Week:

Clearnomics,

Bureau of Labor Statistics

Statistic of the Week:

CNBC.com, The Economist

Global Perspective:

The Economist

Commentary:

1. Bloomberg

2. Bloomberg

3. Bloomberg

4. MarketWatch.com

5. Bloomberg

6. Barron’s

7. Investor’s Business Daily

8. Investor’s Business Daily